Why More People Are Working Harder, Earning More, and Still Falling Behind

Why More People Are Working Harder, Earning More, and Still Falling Behind

For generations, poverty was often associated with unemployment, homelessness, or a lack of opportunity.

Today, a new reality is emerging.

Many Americans have jobs.

Many have degrees.

Many own homes.

Many earn salaries that previous generations would have considered comfortable.

Yet millions still feel financially trapped.

They work full-time.

They pay their bills.

They contribute to retirement accounts when possible. Yet month after month, they find themselves asking the same question:

“Why does it still feel like I’m falling behind?”

This is the new American poverty nobody talks about.

📊 The Numbers Tell a Different Story

More income is not necessarily translating into more financial security.

According to multiple national surveys, a significant percentage of Americans report living paycheck to paycheck, including households earning six-figure incomes.

At first glance, that seems impossible.

How can someone earning $100,000 or more struggle financially?

The answer is more complicated than income alone.

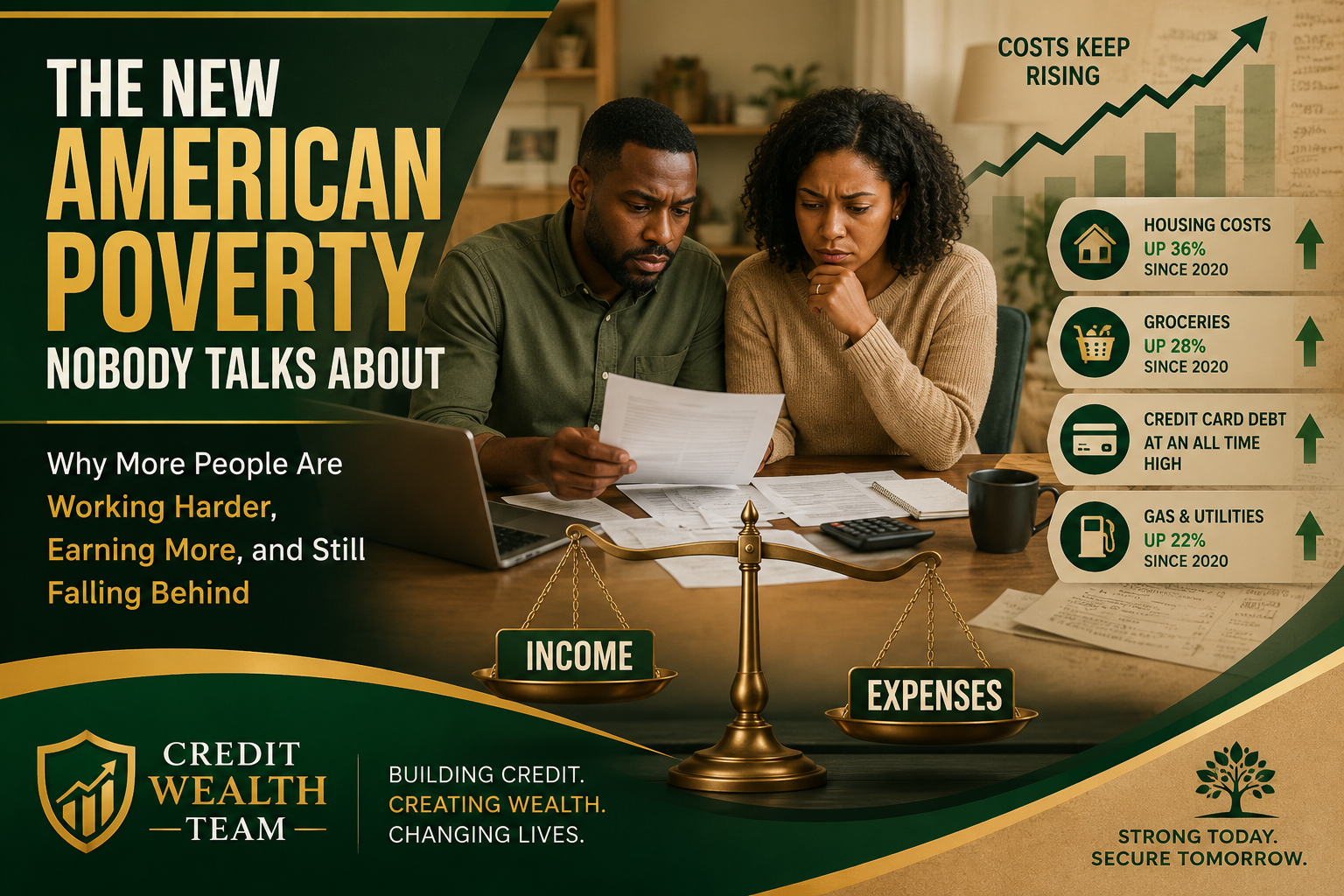

Housing costs have risen dramatically in many parts of the country. Healthcare expenses continue to climb. Insurance premiums increase year after year. Childcare expenses can rival a second mortgage payment. Everyday necessities such as groceries, transportation, and utilities consume a larger share of household budgets than they did just a decade ago.

The result is a growing number of households that appear financially stable from the outside while experiencing significant financial stress behind closed doors.

🏠 The Housing Reality

Summary: Shelter has become one of the largest barriers to financial freedom.

For many families, housing consumes 30% to 50% of monthly income.

In some cities, first-time homebuyers face prices that are several times higher than annual household income. Renters often experience yearly increases that outpace wage growth.

This creates a difficult cycle.

A family may receive a raise at work, only to see the benefit absorbed by higher rent, property taxes, insurance costs, or maintenance expenses.

Income rises.

Expenses rise faster.

Progress feels impossible.

🛒 Inflation’s Lingering Effects

Even when inflation slows, prices rarely return to previous levels.

Many consumers hear reports that inflation is decreasing and wonder why groceries still feel expensive.

The answer is simple.

Inflation slowing does not mean prices are falling.

It means prices are increasing more slowly than before.

A gallon of milk that increased from $3 to $5 does not automatically return to $3 simply because inflation rates decline.

Families continue paying higher prices while wages often struggle to keep pace.

Over time, this creates a silent squeeze on household budgets.

💳 The Credit Trap

Credit can be a powerful tool, but it can also become a survival mechanism.

Many households use credit cards not for luxury purchases but for necessities.

- Unexpected medical bills.

- Vehicle repairs.

- Emergency travel.

- Temporary job loss.

When emergencies occur without adequate savings, credit often fills the gap.

The challenge arises when temporary debt becomes permanent debt.

Interest charges compound. Minimum payments grow. Financial flexibility disappears.

What began as a short-term solution becomes a long-term burden.

😔 The Emotional Cost of Financial Stress

Summary: Financial stress affects far more than bank accounts.

Money problems frequently impact mental health, physical health, relationships, and overall quality of life.

Studies have linked financial stress to:

Increased anxiety

Depression

Sleep disturbances

Relationship conflict

Reduced workplace productivity

Many people suffer in silence because they believe they are alone.

They are not.

The reality is that millions of Americans share similar concerns, even if their social media profiles suggest otherwise.

🎭 The Illusion of Wealth

Looking wealthy and being wealthy are two very different things.

Social media has created unprecedented pressure to appear successful.

Luxury vacations.

New vehicles.

Designer brands.

Large homes.

These images create powerful comparisons.

What viewers often do not see are the loans, credit card balances, and financial obligations supporting those lifestyles.

True wealth is not always visible.

Many financially secure households drive older vehicles, avoid unnecessary debt, and prioritize long-term financial stability over appearances.

💡 What Wealthy Families Often Do Differently

Wealth is frequently built through habits rather than income alone.

While income certainly matters, many financially successful families focus on several core principles:

Maintaining emergency savings

Avoiding high-interest debt

Investing consistently

Living below their means

Protecting their credit profile

Making long-term decisions rather than emotional purchases

These habits may seem simple, but over time they create substantial financial resilience.

🧠 What Credit Wealth Team Readers Can Learn

The new American poverty is not always visible.

It may be your coworker.

Your neighbor.

Your friend.

It may even be someone earning significantly more than the national average.

Financial freedom is not determined solely by income.

It is influenced by spending habits, debt management, credit health, emergency preparedness, and long-term planning.

The goal is not simply to earn more.

The goal is to create a financial foundation strong enough to withstand life’s unexpected challenges.

🔔 Perhaps the greatest financial misconception of our time is the belief that more income automatically creates more security.

For many households, higher earnings have not eliminated financial stress.

They have simply changed its appearance.

The new American poverty is not always homelessness.

It is often hidden behind mortgages, car payments, credit card balances, and rising living expenses.

Understanding this reality is the first step toward changing it.

Because financial dignity is not about how much money you make.

It is about how much control you have over your financial future.

📚

Federal Reserve. (2024). Report on the Economic Well-Being of U.S. Households.

Consumer Financial Protection Bureau. (2024). Making Ends Meet Survey.

U.S. Bureau of Labor Statistics. (2025). Consumer Price Index Summary.

Pew Research Center. (2024). The Financial Pressures Facing Middle-Class Americans.

CNBC. (2024). Why More Americans Are Living Paycheck to Paycheck.